Table Of Content

Results in no way indicate approval or financing of a mortgage loan. Contact a mortgage lender to understand your personalized financing options. Here are a few documents you should gather to help you understand your financial situation and how much house you can afford. This information will also be required when you apply for a pre-approved home loan.

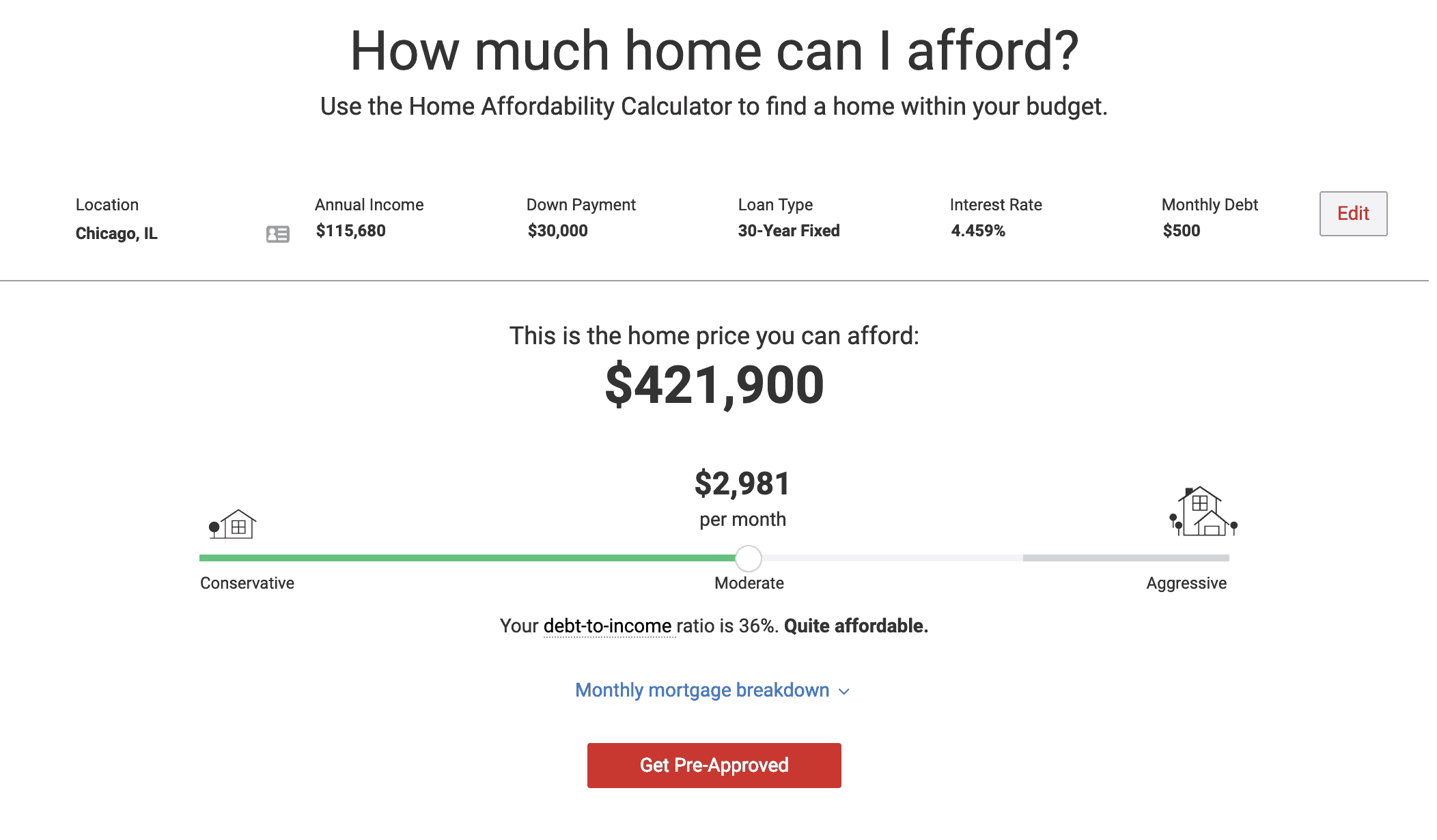

How does your debt-to-income ratio impact affordability?

Home Affordability Calculator - How Much House Can I Afford - realtor.com® - Realtor.com News

Home Affordability Calculator - How Much House Can I Afford - realtor.com®.

Posted: Mon, 26 Jan 2015 18:58:58 GMT [source]

The longer you can stay in a home, the easier it is to justify the expenses of closing costs and moving all your belongings — and the more equity you’ll be able to build. Interest rate - Estimate the interest rate on a new mortgage by checking Bankrate's mortgage rate tables for your area. Once you have a projected rate (your real-life rate may be different depending on your overall financial and credit picture), you can plug it into the calculator.

Calculate your affordability

Explore mortgage options to fit your purchasing scenario and save money. Use the affordability calculator to see how your down payment affects your home affordability estimate and your monthly mortgage payment. Key factors in calculating affordability are 1) your monthly income; 2) cash reserves to cover your down payment and closing costs; 3) your monthly expenses; 4) your credit profile. A good affordability rule of thumb is to have three months of payments, including your housing payment and other monthly debts, in reserve. This will allow you to cover your mortgage payment in case of an unexpected event.

How much house can I afford with an FHA loan?

The loan does not require any down payment, and unlike other loans, it also does not require private mortgage insurance. Depending on your credit score, you may be qualified at a higher ratio, but generally, housing expenses shouldn’t exceed 28% of your monthly income. A fixed rate is when your interest rate remains the same for your entire loan term. An adjustable rate stays the same for a predetermined length of time and then resets to a new interest rate on scheduled intervals.

Eligible active duty or retired service members, or their spouses, might qualify for down payment–free mortgages from the U.S. These loans have competitive mortgage rates, and they don't require PMI, even if you put less than 20 percent down. Plus, there is no limit on the amount you can borrow if you’re a first-time homebuyer with full entitlement. You’ll need to also consider how the VA funding fee will add to the cost of your loan. The major part of your mortgage payment is the principal and the interest. The principal is the amount you borrowed, while the interest is the sum you pay the lender for borrowing it.

Zillow's mortgage calculator gives you the opportunity to customize your mortgage details while making assumptions for fields you may not know quite yet. These autofill elements make the home loan calculator easy to use and can be updated at any point. Use the home affordability calculator to help you estimate how much home you can afford. Conventional loans can come with down payments as low as 3%, although qualifying is a bit tougher than with FHA loans.

Where you live plays a major role in what you can spend on a house. For example, you’d be able to buy a much bigger piece of property in St. Louis than you could for the same price in San Francisco. If you live in a town where transportation and utility costs are relatively low, for example, you may be able to carve out some extra room in your budget for housing costs. While it's true that a bigger down payment can make you a more attractive buyer and borrower, you might be able to get into a new home with a lot less than the typical 20 percent down. Some programs make mortgages available with as little as 3 percent or 3.5 percent down, and some VA loans are even available with no money down at all.

Your lender also might collect an extra amount every month to put into escrow, money that the lender (or servicer) then typically pays directly to the local property tax collector and to your insurance carrier. Get pre-qualified by a lender to see an even more accurate estimate of your monthly mortgage payment. APR (%) is a number designed to help you evaluate the total cost of a mortgage.

The mortgage interest rate is the amount charged by a lender in exchange for loaning money to a buyer. It is expressed as a yearly percentage of the total loan amount but is calculated into the monthly mortgage payment. Home prices have been on a rollercoaster ride in recent years and are still very high, as are mortgage rates. It’s enough to make you wonder whether now is even a good time to buy a house. It’s important to focus on your personal situation rather than thinking about the overall real estate market.

Other factors, such as our own proprietary website rules and whether a product is offered in your area or at your self-selected credit score range, can also impact how and where products appear on this site. While we strive to provide a wide range of offers, Bankrate does not include information about every financial or credit product or service. Annual property tax is a tax that you pay to your county, typically in two installments each year.

Down payment - The down payment is money you give to the home's seller. At least 20 percent down typically lets you avoid mortgage insurance. VA loans are partially backed by the Department of Veterans Affairs, allowing eligible veterans to purchase homes with zero down payment (in most cases) at competitive rates. Find out what you'd owe each month given a specific purchase price, interest rate, length of your loan, and the size of your down payment. Gross monthly income is the total amount of money you earn in a month before taxes or deductions. Adjustable-rate mortgages (ARMs) have interest rates that can change over time.

No comments:

Post a Comment